Why aren’t pensions totes amazeballs?

To paraphrase Oscar Wilde: “Pensions are wasted on the Young”.

The Question is Why?

A mini-survey was carried out on 67 individuals in different industry sectors under the age of 35 with some of the findings coming as a surprise. The purpose of this survey was to derive an idea of the opinions of those individuals on saving for their future.

The findings indicated the youth of today are focused on ‘living for the now’. However, when asked about their idea of what retirement means, they think of a time which is fun, filled with holidays and, specifically, not having to work. The State pension nowadays is less than half the current average salary of those in employment in this age group, which poses the question ‘how do they expect to fund for this expected lifestyle?’

The results of the survey reveal that the majority of these individuals do not have a pension scheme. Just fewer than half the participants claim that their employer company does not provide a pension scheme. It was surprising to note that a large amount of these individuals stated they have not been approached by their employer and advised of the availability of a mechanism to begin saving for their retirement. It is a mandatory requirement that all employers offer a company scheme or a standard PRSA, this leads us to believe the availability of such schemes are not sufficiently promoted.

When the sample was asked if they would save themselves for retirement, responses were negative, consisting of phrases such as “too costly”, “can’t afford to” and “maybe in the future”.

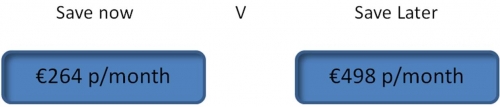

The lack of saving earlier in life will mean a significant amount of stress will be placed on the amount to be contributed to make up the same expected salary for retirement. Take for example, two people, both earning €40,000 per annum and expecting to get a pension of 68% of that salary (€24,600). One decides to begin saving at 26, the other at 41. To achieve the same outcome they will both have very different contribution amounts:

It is important to focus on providing guidance to younger people to invest in their pension as this will benefit them later in life when they may need more disposable income.

This issue was discussed directly with some of the participants who worked in financial services and who were therefore professionally aware of the need for pension savings but had not yet undertaken any pension planning themselves.

Whilst validating some of the comments outlined above these participants also offered some comments on the approach of the industry itself to the issue:

“If pensions are so important why do they appear at the end of the Manual?”

“When we were presented with details of the financial planning pyramid – pensions always appeared at the bottom”.

Portions of the survey undertaken focused on particular features that could be included in pension products to make them of more interest to young people. This will form the subject of a later article.

However both the general comments and the specific feedback from those in the industry highlighted a number of points about communication:

- We as an industry are not clear in the message we give to young people on this topic

- Whilst employers are obliged to provide access to a pension mechanism, greater work needs to be done around communicating this to the younger audience

The under 35s are often referred to as the “Apple Generation”. This reflects the significance of technology and social media to their everyday lives. Perhaps the real message coming from this survey is that greater use of such tools is necessary if we want to communicate fully to this generation.

By Emma Herrity, Trustee Administrator, Independent Trustee Limited.

*Please note this content is the view of the author and not of Independent Trustee Company